Reimagine Delinquency Management

Predictive, Proactive, Progressive

An eBook by Infosys and FICO

Infosys Aster is an AI-amplified marketing suite, tailored for marketers. It helps them deliver engaging brand experiences, enhance marketing efficiency, and accelerate effectiveness for business growth. Combining the generative AI capabilities...

Solving the Delinquency Dilemma

A Customer-centric Solution for Pre-delinquency

Becomes the Need of the Hour

Introducing Infosys Decisioning-as-a-Service (DaaS)

To discover how DaaS can help your organization achieve its financial and experiential goals, please feel free to reach out to askus@infosys.com

The pandemic had a domino impact on the economic landscape.

Relaxed credit standards often lead to increased borrowing and debt, but rising interest rates and financial strain eventually trigger a surge in delinquencies, prompting tighter lending. Even years after the pandemic, delinquencies remain high.

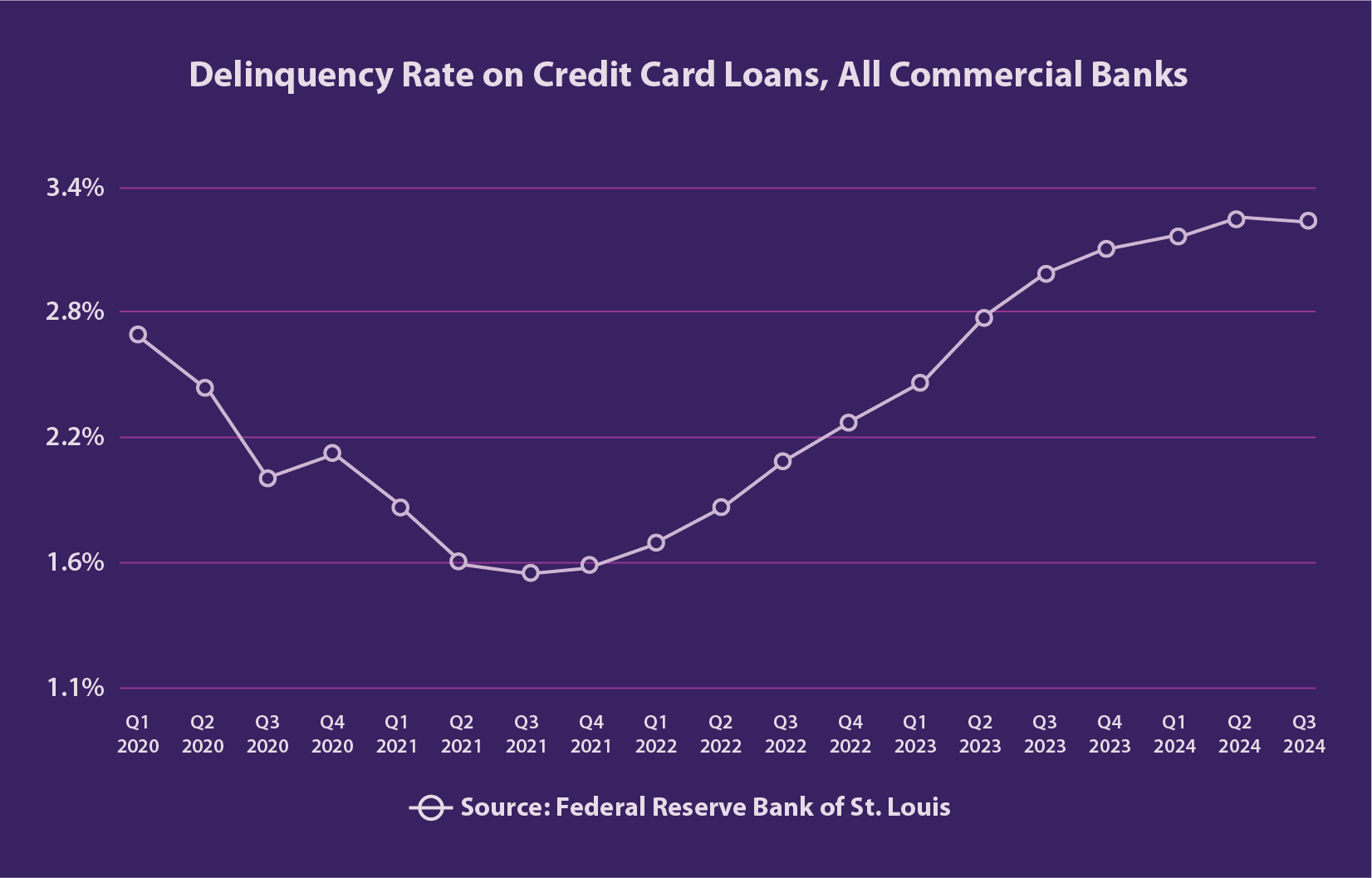

Credit card delinquencies doubled from 1.6% in 2021 to 3.4% in 2024, reaching a four-year high.

Banks that leverage advanced decision infrastructure can turn this challenge into an advantage, strengthening customer relationships, delivering personalized offers, and building lasting loyalty through data-driven strategies.

This eBook will discuss how we got here and what lenders can do about it.

Delinquency remains the most pressing challenge. Since January 2020, unit delinquency rates have increased by over 50%, while balance delinquency rates have risen at an even steeper pace. Notably, balance delinquencies have surged by 51% over the past two years, yet this is only one part of a broader and growing concern.

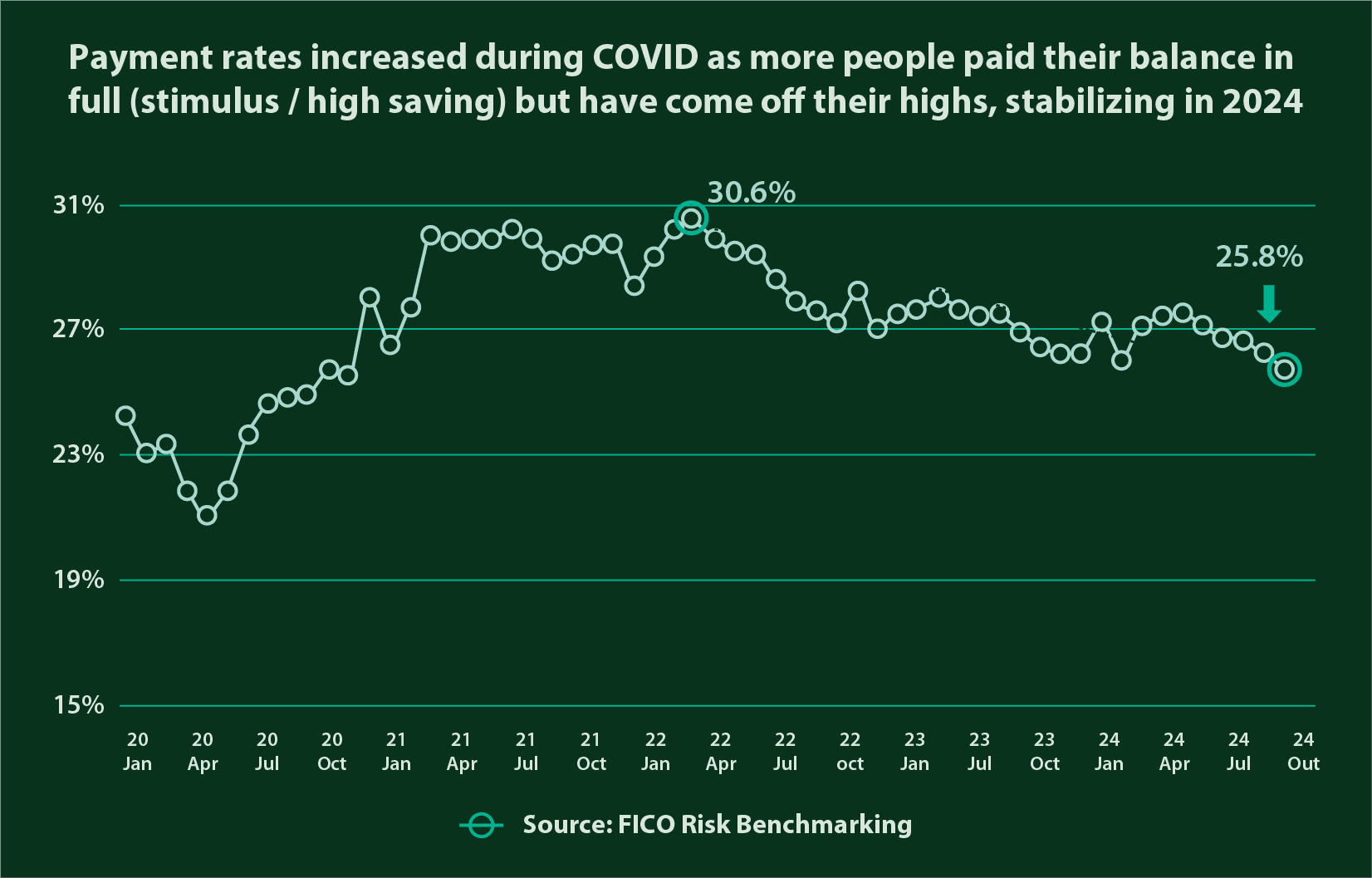

Payment rates are also trending downward.

Initially buoyed by heightened savings and government support during the COVID-19 pandemic, payment rates surged. However, they have steadily declined since peaking in 2022. While it remains uncertain whether this trend will persist, lenders must be prepared for a sustained environment characterized by rising delinquencies and declining payment rates.

How can banks monitor and manage these concerns before they become problems?

Lenders must first address delinquencies by gaining a clear understanding of their underlying drivers. Several factors contribute to the upward trend in delinquencies, including:

Lenient credit standards during the pandemic

Government stimulus in the recovery phase

The post-recovery rise in inflation

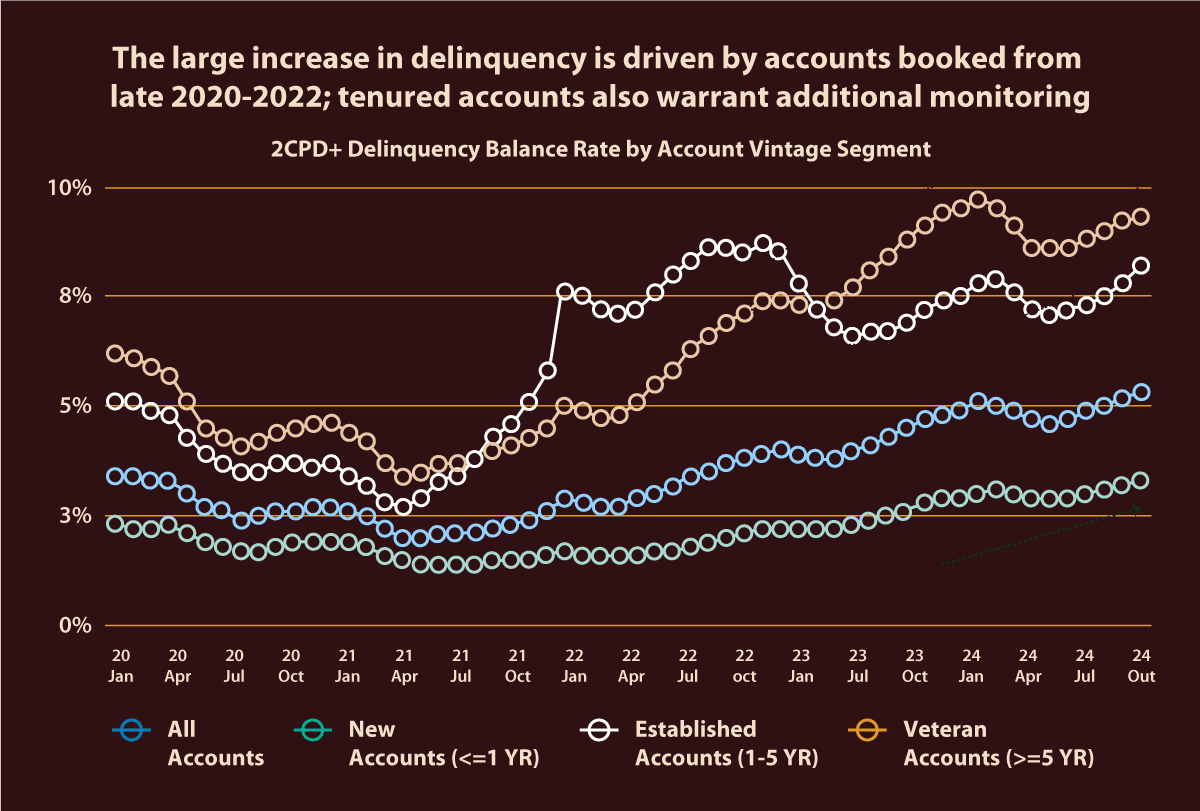

Even longstanding account holders are now at risk of delinquency, pointing to broader economic pressures. New tariffs, recession concerns, and ongoing uncertainty suggest delinquency rates may stay high in the near term.

A challenge and an opportunity With macroeconomic conditions unlikely to ease delinquency rates and high household debt, many lenders are concerned about their balance sheets. However, those willing to take decisive action have an opportunity to implement targeted, timely, and effective data-driven interventions. The following sections explore how this can be done.